Table of Contents |

An annuity is a type of multi-period investment where there is a certain principal deposited and then regular payments made over the course of the investment. The payments are all a fixed size.

EXAMPLE

A car loan may be an annuity. In order to get the car, you are given a loan to buy the car. In return, you make an initial payment (down payment), and then payments each month of a fixed amount.There is still an interest rate implicitly charged in the loan. The sum of all the payments will be greater than the loan amount, just as with a regular loan, but the payment schedule is spread out over time.

As a bank, there are three advantages to making the loan an annuity:

Since annuities, by definition, extend over multiple periods, there are different types of annuities based on when in the period the payments are made:

The future value of an annuity is the sum of the future values of all of the payments in the annuity. It is possible to take the FV of all cash flows and add them together, but this isn’t really pragmatic if there are more than a couple of payments. If you were to manually find the FV of all the payments, it would be important to be explicit about when the inception and termination of the annuity is.

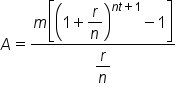

For an annuity-due, the payments occur at the beginning of each period, so the first payment is at the inception of the annuity, and the last one occurs one period before the termination.

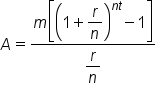

For an ordinary annuity, however, the payments occur at the end of the period. This means the first payment is one period after the start of the annuity, and the last one occurs right at the end. There are different FV calculations for annuities-due and ordinary annuities because of when the first and last payments occur.

There are some formulas to make calculating the FV of an annuity easier. For both of the formulas we will discuss, you need to know the payment amount (m, though can be written as pmt or p), the interest rate of the account the payments are deposited in (r, though sometimes i), the number of periods per year (n), and the time frame in years (t).

The formula for an ordinary annuity is as follows:

In contrast, the formula for an annuity-due is as follows:

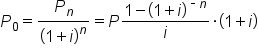

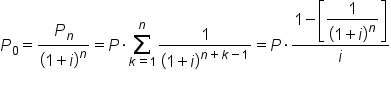

The Present Value (PV) of an annuity can be found by calculating the PV of each individual payment and then summing them up. As in the case of finding the Future Value (FV) of an annuity, it is important to note when each payment occurs.

Annuities-due have payments at the beginning of each period, and ordinary annuities have them at the end. Recall that the first payment of an annuity-due occurs at the start of the annuity, and the final payment occurs one period before the end. The PV of an annuity-due can be calculated as follows:

An ordinary annuity has annuity payments at the end of each period, so the formula is slightly different than for an annuity-due. An ordinary annuity has one full period before the first payment (so it must be discounted) and the last payment occurs at the termination of the annuity (so it must be discounted for one period more than the last period in an annuity-due). The formula is:

Both annuities-due and ordinary annuities have a finite number of payments, so it is possible, though cumbersome, to find the PV for each period. For perpetuities, however, there are an infinite number of periods, so we need a formula to find the PV. The formula for calculating the PV is the size of each payment divided by the interest rate.

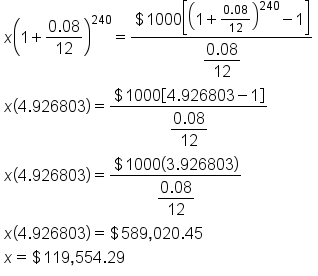

Suppose you have won a lottery that pays $1,000 per month for the next 20 years. But, you prefer to have the entire amount now. If the interest rate is 8%, how much will you accept?

Consider for argument purposes that two people, Mr. Cash and Mr. Credit, have won the same lottery of $1,000 per month for the next 20 years. Now, Mr. Credit is happy with his $1,000 monthly payment, but Mr. Cash wants to have the entire amount now. Our job is to determine how much Mr. Cash should get. We reason as follows: if Mr. Cash accepts x dollars, then the x dollars deposited at 8% for 20 years should yield the same amount as the $1,000 monthly payments for 20 years. In other words, we are comparing the future values for both Mr. Cash and Mr. Credit, and we would like the future values to be equal.

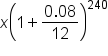

Since Mr. Cash is receiving a lump sum of x dollars, its future value is given by the lump sum formula:

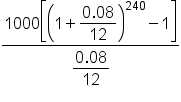

Since Mr. Credit is receiving a sequence of payments, or an annuity, of $1,000 per month, its future value is given by the annuity formula:

The only way Mr. Cash will agree to the amount he receives is if these two future values are equal. So we set them equal and solve for the unknown:

So, if Mr. Cash takes his lump sum of $119,554.29 and invests it at 8% compounded monthly, he will have $589,020.45 in 20 years.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM "BOUNDLESS FINANCE" PROVIDED BY LUMEN LEARNING BOUNDLESS COURSES. ACCESS FOR FREE AT LUMEN LEARNING BOUNDLESS COURSES. LICENSED UNDER CREATIVE COMMONS ATTRIBUTION-SHAREALIKE 4.0 INTERNATIONAL.