Table of Contents |

FIFO is an inventory valuation method, which stands for First In First Out:

As an inventory valuation method, FIFO helps to provide information about cost of goods sold and ending inventory. Under FIFO, goods that were purchased first are the first to be sold, meaning goods are assumed to be sold oldest to newest. A benefit to using FIFO is that it resembles the physical flow of goods.

EXAMPLE

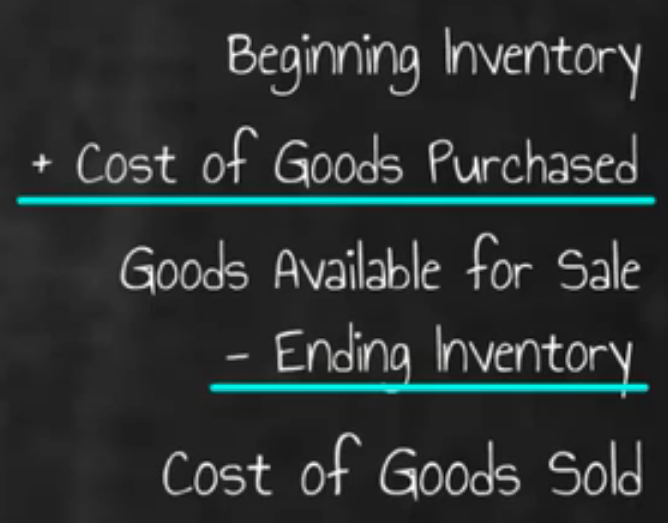

Grocery stores or electronic stores, for example, want the inventory that they purchased first--their oldest products--to be sold first. In the case of grocery stores, they want to sell the oldest merchandise first so that their food doesn't spoil.Next we will discuss FIFO and cost of goods sold. Remember, the cost of goods sold calculation starts with beginning inventory, then we add cost of goods purchased, which gives us goods available for sale. Then, we subtract out ending inventory, which equals cost of goods sold.

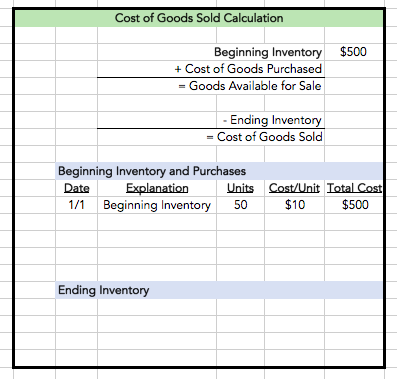

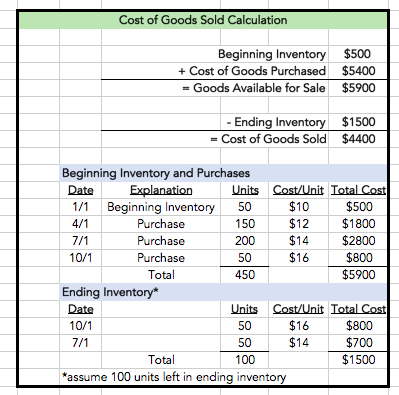

Let's walk through an example of calculating cost of goods sold using the inventory valuation method of FIFO. Below you will see a spreadsheet outlining the cost of goods sold calculation. We will begin with the first line, beginning inventory. Beginning inventory is pulled from our balance sheet or from our trial balance. You can also see there is a schedule, detailing beginning inventory and purchases.

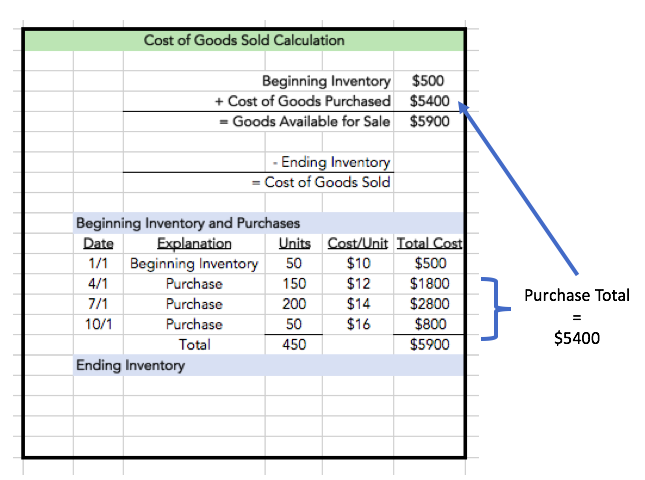

Once we have plugged in beginning inventory, we need to determine cost of goods purchased. If you look at the detail of all the purchases made, you can see that we made three purchases throughout the year.

We can take the total of those purchases, which is $5,400, and drop that into the schedule, which means we now have total goods available for sale of $5,900. Note that this is the total of beginning inventory plus all of the purchases.

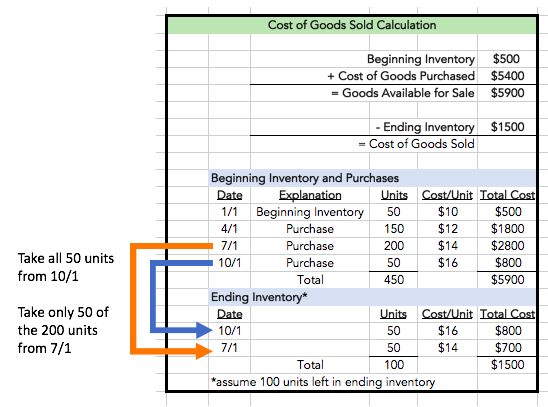

Now we need to know what our ending inventory is. If you look at the ending inventory schedule below, we're going to make the assumption that we have 100 units left in our ending inventory.

So, if we're using FIFO and we have 100 units left, what does that mean? Which units are left in inventory? Under FIFO--First In First Out--, the oldest units (the units that came in first) were the first units to be sold. So when we are looking at ending inventory, we will be left with the newest units as our inventory. Start with the most recent purchase and work our way back.

If we have 100 units left, we know that we can take 50 units from the purchase made on the most recent purchase of 10/1, and then we can take another 50 units from the purchase made on July 1. This means that our ending inventory, 100 units, is $1,500.

Then, we take that number, and drop it into our cost of goods sold calculation. We subtract out our ending inventory to give us cost of goods sold.

IN CONTEXT

Consider the following table:

Beginning Inventory and Purchases Purchased Units Unit Cost Total Cost Beginning Inventory 100 $5 $500 September 120 $6 $720 October 140 $7 $980 November 130 $8 $1,040 Units Available For Sale 490 $3,240 Ending Inventory Units on Hand 290 Cost of Units on Hand $ Units Sold 200 Cost of Goods Sold $

Using the FIFO method and the information in this table, what is the cost of units on hand and cost of goods sold during this period?

First, find the ending inventory. With FIFO, the ending inventory is going to be our newest units. We have 290 items on hand, which means we will take all 130 units from November, all 140 units from October, and 20 units from September:

The ending inventory, or cost of units on hand, for these 290 items is $2,140. Now we can subtract this value from the goods available for sale to find the cost of goods sold.

The cost of goods sold using FIFO method is $1,100.

Beginning Inventory and Purchases Purchased Units Unit Cost Total Cost Beginning Inventory 100 $5 $500 September 120 $6 $720 October 140 $7 $980 November 130 $8 $1,040 Units Available For Sale 490 $3,240 Ending Inventory Units on Hand 290 Cost of Units on Hand $2,140 November 130 $8 $1,040 October 140 $7 $980 September 20 $6 $120 Units Sold 200 Cost of Goods Sold 1,100 September 100 $6 $600 Beginning Inventory 100 $5 $500

Source: Adapted from Sophia instructor Evan McLaughlin.