Table of Contents |

In review, the expanded income statement starts with sales minus cost of goods sold equals gross profit. We then subtract out operating expenses to arrive at income from operations. Finally, we add other revenues or subtract other expenses to equal net income.

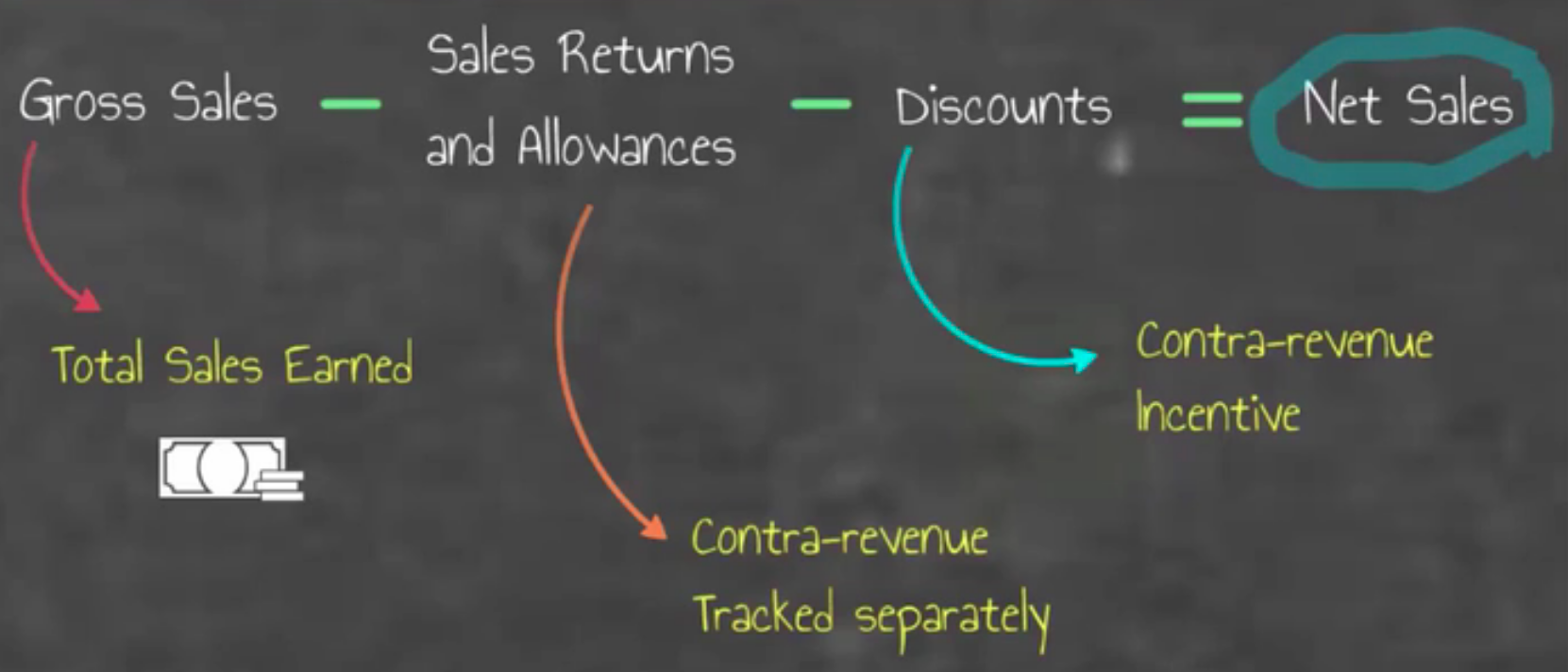

We can further break down the expanded income statement by taking the sales piece and looking at gross sales and net sales, separately calculating net sales.

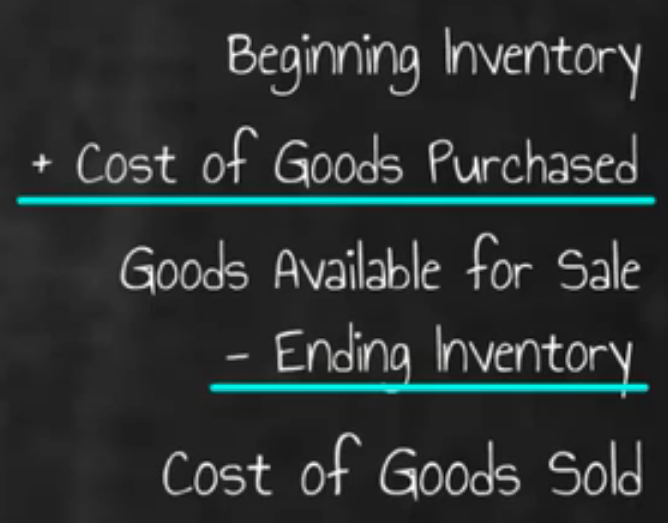

We can also break down the cost of goods sold piece. Cost of goods sold is a component of cost of goods purchased, which is going to give us goods available for sale. Then, we can calculate the cost of goods sold figure. Therefore, the whole process is made up of a few different calculations.

Now we're going to break down our sales, looking at gross sales and calculating our net sales, through the expanded sales calculation.

Starting with gross sales, we subtract out sales returns and allowances, and subtract out discounts, to equal net sales.

Again, the expanded sales calculation is gross sales minus sales return and allowances, minus discounts, equals net sales.

We can also expand the cost of goods sold calculation. Starting with our beginning inventory, we add cost of goods purchased to give us the goods available for sale. From there, we subtract out ending inventory to provide the cost of goods sold.

However, we can go even further by breaking down the cost of goods purchased piece of the calculation, starting with purchases, minus discounts, minus purchase returns and allowances to equal net purchases. Next, we would add freight-in, which is the shipping cost to bring the inventory to us, to give us the total cost of goods purchased. This is how we calculate cost of goods purchased, which we can now plug into the cost of goods sold calculation.

Now that we have discussed the formulas and calculations involved, let's look at an example of calculating cost of goods sold, as well as cost of goods purchased.

As you can see, we start at the top with beginning inventory, $500,000, which we would pull from our accounting information.

To this beginning inventory, we add cost of goods purchased. Well, how do we figure out cost of goods purchased? We have to go down to the cost of goods purchased calculation.

Starting with our purchases, we subtract out purchase returns and allowances, and subtract out purchase discounts, which provides us with net purchases. Then, once we have our net purchases, we add freight-in, or those shipping costs that we incurred getting the merchandise to us, to give us the total cost of goods purchased, $181,000.

Now we can take the cost of goods purchased, that $181,000, and bring it up to the cost of goods sold calculation. We input it into the cost of goods sold purchased, then we can add our beginning inventory.

This sum equals our goods available for sale: beginning inventory plus cost of goods purchased equals goods available for sale.

Finally, we subtract out our ending inventory--what we have left on hand--to equal the cost of goods sold.

Source: Adapted from Sophia instructor Evan McLaughlin.