Table of Contents |

The time value of money framework says that money in the future is not worth as much as money in the present. Investors would prefer to have the money today because then they are able to spend it, save it, or invest it right now instead of having to wait to be able to use it.

The difference between what the money is worth today and what it will be worth at a point in the future can be quantified. The value of the money today is called the present value (PV), and the value of the money in the future is called the future value (FV).

Another common term for finding present value (PV) is discounting . Discounting is the procedure of finding what a future sum of money is worth today. As you know from the previous sections, to find the PV of a payment, you need to know the future value (FV), the number of time periods in question, and the interest rate. The interest rate, in this context, is more commonly called the discount rate.

The discount rate is the term for the cost of not having the money today.

EXAMPLE

If the interest rate is 3% per year, it means that you would be willing to pay 3% of the money to have it one year sooner.It also represents some cost (or group of costs) to the investor or creditor. The sum of these costs amounts to a percentage which becomes the interest rate (plus a small profit, sometimes).

Here are some of the most significant costs from the investor/creditor’s point of view:

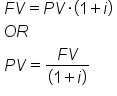

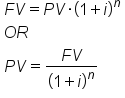

The PV and the discount rate are related through the same formula we have been using for a future value of a single payment. The equation can be rearranged to solve for PV of a single amount of money. That is, it tells you what a single payment is worth today, but not what a series of payments is worth today (that will come later). In order to find the PV, you must know the FV, i, and n.

With single-period investments, the concept of the time value of money is relatively straightforward. The future value is simply the present value applied to the interest rate compounded one time. So, by definition, the variable for time, n, is equal to one. If we update the formula with this information, and rearrange it so we are solving for PV, this simply means that the PV is FV divided by 1+i.

There is a cost to not having the money for one year, which is what the interest rate represents. Therefore, the PV is i% less than the FV.

When investing, the time value of money is a core concept investors simply cannot ignore. A dollar today is valued higher than a dollar tomorrow, and when utilizing the capital, it is important to recognize the opportunity cost involved in what it could have been invested in instead.

With multi-periods in mind, interest begins to compound. Compound interest simply means that the interest from the first period is added to the future present value, and the interest rate the next time around is now being applied to a larger amount. This turns into an exponential calculation of interest, calculated as follows:

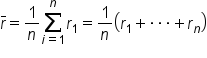

This means that the interest rate of a given period may not be the same percentage as the interest rate over multiple periods (in most situations). A useful tool at this point is a way to create an average rate of return over the life of the investment, which can be derived with the following:

Finding the present value (PV) of an amount of money is finding the amount of money today that is worth the same as an amount of money in the future, given a certain interest rate.

Calculating the present value (PV) of a single amount is a matter of combining all of the different parts we have already discussed. But first, you must determine whether the type of interest is simple or compound interest. If the interest is simple interest, you plug the numbers into the simple interest formula. If it is compound interest, you can rearrange the compound interest formula to calculate the present value.

Once you know these three variables, you can plug them into the appropriate equation. If the problem doesn’t say otherwise, it’s safe to assume the interest compounds. If you happen to be using a program like Excel, the interest is compounded in the PV formula. Simple interest is fairly rare.

IN CONTEXT

Suppose you would like to have $1,000 dollars in an account after three year’s time. If the account earns 5% compounded interest yearly, how much would you have to deposit today?

Deciding how much to deposit today is the same as the present value. Since we know the future value ($1,000), the timing (3 years), and the interest rate (5%), we can find the present value using the following formula:

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM "BOUNDLESS FINANCE" PROVIDED BY LUMEN LEARNING BOUNDLESS COURSES. ACCESS FOR FREE AT LUMEN LEARNING BOUNDLESS COURSES. LICENSED UNDER CREATIVE COMMONS ATTRIBUTION-SHAREALIKE 4.0 INTERNATIONAL.