Table of Contents |

Current liabilities show a company's obligation to pay debts to others within one year or the operating cycle, whichever is shorter; the are they company's short-term debt obligations.

There are several types of current liabilities:

Short-term notes payable are written agreements to pay a defined sum of money at a specified future date. The key phrase of this definition is "at a specified future date."

Because they are short-term notes payable, they are going to be due within less than a year. So, that specified future date mentioned above is going to be within less than a year.

Short-term notes payable are also interest bearing, so there will be a stated interest rate for our short-term notes payable.

Short-term notes payable are used for things like purchasing equipment, for instance. It's a way to finance that purchase if the company doesn't have the cash on hand immediately.

Let's look at some examples of establishing notes payable.

EXAMPLE

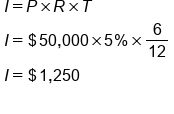

ABC Company borrows $50,000 from National Bank on January 1, 2012. They sign a 5%, 6-month note.

EXAMPLE

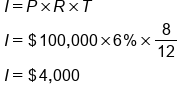

XYZ Company borrows $100,000 from Local Bank on January 1, 2012. XYZ Company signs a 6%, 8-month note.

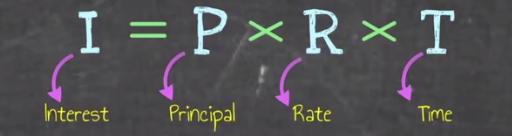

Now let's turn our attention to interest payable. The calculation for determining interest payable reads I equals P times R times T.

In this formula, I stands for interest, P stands for principal, or the amount of the loan, R is the stated rate in the written agreement, and T is the length of time that the note is outstanding.

Now, the easiest way to illustrate interest payable is to look at some examples. We'll use the same two examples from above, but this time we're going to calculate interest payable.

EXAMPLE

ABC Company borrows $50,000 from National Bank and they sign a 5%, 6-month note. Therefore, principle times rate times time gives us interest for this example of $1,250.

Therefore, principle times rate times time gives us interest for this example of $1,250.

EXAMPLE

XYZ Company borrows $100,000 from Local Bank on January 1, 2012. XYZ Company signs a 6%, 8-month note.

Source: Adapted from Sophia instructor Evan McLaughlin.