Table of Contents |

Organizations have a few options available when it comes to finding funding for their operations. From debt options, such as taking out loans or offering long-term corporate bonds, to equity, such as preferred and common stock, larger organizations tend to find a balance between these options that is optimized for the best possible weighted average cost of capital (WACC) to operate at the scale that creates the best revenue opportunity.

WACC is a useful calculation, as it shows management what the cost of borrowing capital is overall. This overall cost of capital can then be a minimum required return on any new operation.

EXAMPLE

If it will cost 8% in capital costs to fund a project that creates 10% in profit, the organization can confidently borrow capital to fund this project. If the project would only turn 8% profit, the firm would have a difficult decision. If the project would turn 6% profit, it is quite easy to strategically argue against the new project.Calculating the cost of capital is actually quite a simple equation. Most firms are only receiving capital from either debt or equity, though there can be quite a few inputs to each of these subheadings. What this means is that the overall percentage of the business that is funded by debt must be multiplied by the cost of debt, while similarly the percent funding of equity must be multiplied by the cost of equity, and then added together. This can also be applied to the corporate tax rate in a given country of operation. This is written out as follows:

The cost of debt (Rd) is usually fixed, based on the terms of a given bond or loan contract. As a result, the cost of debt is usually both certain and predictable. The cost of equity (Re) is a little bit more complex, as it is speculative and often determined (to some degree) by investor behavior. The capital asset pricing model (CAPM) is a traditional approach to determining the cost of equity.

To calculate the weighted average cost of capital (WACC) we must take into account the weight of each component of a company’s capital structure.

Referencing the formula from above:

The “weighting” varies based on how the company finances its activities. If the value of a company’s debt exceeds the value of its equity, the cost of its debt will have more “weight” in calculating its total cost of capital than the cost of equity. If the value of the company’s equity exceeds its debt, the cost of its equity will have more "weight."

Since we are measuring expected cost of new capital, the calculation of weighted average cost of capital usually uses the market values of the various components rather than their book values. These may differ significantly.

Market value is the price at which an asset would trade in a competitive auction setting. It is the true underlying value of an asset according to theoretical standards. It is a distinct concept from market price, which is the price at which one can transact. For market price to equal market value, the market must be efficient and rational. Market value also requires the element of “special value” to be disregarded. Special value refers to a synergy that may exist between two parties that makes the fair price of a transaction higher.

Book value refers to the value of an asset according to the account balance present on the balance sheet of a company. The balance sheet is a summary of the financial balances of a company and is often described as a snapshot of a company’s financial condition. An asset’s initial book value is its actual cash value or its acquisition cost. Cash assets are recorded or “booked” at actual cash value. Assets such as buildings, land, and equipment are valued based on their acquisition cost, which includes the actual cash cost of the asset, plus certain costs tied to the purchase of the asset, such as broker fees.

When pursuing financing, organizations encounter a variety of factors that impact the weighted average cost of capital. Some of these factors are within the firm’s strategic control, while others are external forces outside the firm’s control.

As a financial professional or upper level strategist, understanding what capital structure options are available to a firm plays a critical role in financial management.

Capital structure refers to the way in which an organization finances operations. This is generally illustrated via a balance sheet, where the overall assets are offset by the capital structure of liabilities and equity. It is through the decisions to acquire various forms of debt and equity that an organization can derive a weighted average cost of capital (WACC) that is sustainable within the context of organizational profitability. If the cost of capital is higher than the returns from those investments, the organization lacks the profitability required to justify itself.

In the WACC equation, the first segment is measuring the cost of equity coupled with the percentage of the capital structure that is funded by equity. The second segment is making the same calculation, but this time with the cost of debt and the relative percentage of capital structure which is funded via this source. The final segment (1 – t) is the application of a corporate tax rate (depending on the country of operation).

Another important decision made by financial professionals in relation to the cost of capital revolves around the required rates of return of various projects. Investing capital into an operation always incurs the opportunity cost of investing in something else. As a result, organizations can control their operations by measuring and projecting the rate of return on each project, and investing strategically in the most profitable projects.

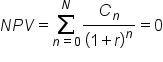

An internal rate of return (IRR) calculation can be useful when doing this. The IRR is going to look at the net present value (NPV) of a given project, and calculate it for a break-even point (i.e., set the equation to zero, when taking cost into account). By doing so, the organization can identify the anticipated rate of return on the project. Take a look at the equation below:

In this equation:

When organizations begin weighing the weighted average cost of capital (WACC) and determining overall capital structure, there are some factors that are within the control of the organization, and some external factors that are not. When it comes to projecting the cost of capital, it is useful to assess some of the external factors that may influence the overall cost.

| External Factors | Description |

|---|---|

| Interest Rates | Interest rates fluctuate for a wide variety of reasons, and are a primary tool of monetary policy. Governments and central banks often make alterations to interest rates as a result of investment, unemployment, inflation, and other broader economic factors. Altering interest rates can impact the spending, borrowing, and investing habits within an economy, and therefore tend to fluctuate for economic purposes. |

| Inflation | Related to interest rates, and a direct impact upon interest rate change, is the natural inflation or deflation of the currency being borrowed or lent. Organizations must take into account the time value of money as it pertains to that capital’s actual alterations in value, which is firmly outside the control of the organization. |

| Market Fluctuations | 2008 is a prime example of how market forces can drastically impact equity. As markets rise and fall, the cost of capital, as well as the perceived market risk (systematic risk), will naturally and relatively unpredictably fluctuate. When utilizing markets as a source of funding, the intrinsic risk of the market itself is outside of the control of the organization. |

| Corporate Tax | Depending upon the region of operation, tax implications may have a significant impact on the cost of capital. In many jurisdictions, debt and interest on equity may receive certain tax breaks. Investors may also encounter taxes on returns on their investments and tax on dividends, impacting the perceived risk and return ratio of a prospective investor. Profit beyond the cost of expenses and capital will be taxed as well, which impacts the overall weighted average cost of capital. |

| Other Factors | The cost of capital is largely a simple trade-off between the time value of money, risk, return, and opportunity cost. Any external factors in the form of opportunity costs or unexpected risks can impact the overall cost of capital. |

The weighted average cost of capital is the minimum return that a company must earn on an existing asset base. This means that, when calculated, WACC will produce a rate equivalent with the current level of risk present in a company’s activities. However, some new ventures will require taking on risks outside of the company’s current scope.

In this case, adjustments will need to be made to the WACC in order to account for the differing level of risk. If the risk is very different, the company’s current WACC may be sidestepped altogether in favor of a WACC typical for companies with similar investments. It is possible to make such adjustments by figuring the differing risk into the company’s beta.

The beta coefficient, expressed as a covariance, is the risk of a new project in relation to the risk of the market as a whole. A company itself will be considered, for investment purposes, as a “portfolio of assets,” and its beta coefficient will represent the weighted average of each “asset’s” beta. Therefore, if a new project of differing risk is undertaken, the beta for that project will be weighted into the company’s overall cost of capital.

EXAMPLE

If the project is twice as sensitive to fluctuations in the market as the company as a whole, then the project’s beta should be twice that of the company during the valuation process. This will increase the risk premium on the project and its cost of equity and subsequently the weighted average cost of capital. This increase in cost of capital will devalue the company’s stock, unless this increase was offset by a higher expected rate of return.The WACC is a common and highly useful approach to determining how much it will cost (as a percentage) to borrow money in order to fund a given operation or project. This overall cost of borrowing capital is a great tool for financial professionals, who would like to understand how much a project will cost, and how much it will provide in return. The overall goal is to maintain a certain level of profitability when it comes to making investments in organizational projects.

As a model, the WACC has quite a few advantages. Generally speaking, this process will take into account the differences between the cost of debt and the cost of equity in a given calculation. This allows the firm to understand how much a project funded fully by debt would differ in terms of capital costs than a project that requires a great deal of equity as well (hint: debt is almost always cheaper).

It also takes into account the time value of money, normalizing cash flows for present value.

Another advantage of this calculation is the simplicity of it. Upper management can quickly look at the WACC for a given project, and compare that to the forecast of the profitability.

No forecast is perfect, however. All financial professionals and upper management executives must understand the drawbacks of WACC (along with those of virtually every attempt to project future costs and profits with present and past data).

The simplest problem with the calculation are the assumptions it relies on. These can include:

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM "BOUNDLESS FINANCE" PROVIDED BY LUMEN LEARNING BOUNDLESS COURSES. ACCESS FOR FREE AT LUMEN LEARNING BOUNDLESS COURSES. LICENSED UNDER CREATIVE COMMONS ATTRIBUTION-SHAREALIKE 4.0 INTERNATIONAL.