Table of Contents |

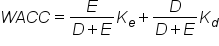

When financing a new project, business, or operation, organizations can utilize both equity and debt to create a balanced weighted average cost of capital. One of the primary differences between equity and debt pertains to risk, and the impact that risk has on the cost of capital. To understand the role of debt, and how the cost of debt impacts overall cost of capital, the weighted average cost of capital equation is a useful data point:

When an organization borrows capital from outside lenders, the interest on these loans is called debt. The variables involved in a debt transaction are fairly simple:

The risk-free rate (or Rf) is externally determined from the general market, and is described as the overall cost incurred due to the time value of money with no risk whatsoever involved. This is usually derived from a government treasury bond, as it is the investment asset in most markets with the lowest possible rate of risk. Tax rates are set externally as well, and are concrete.

The credit risk rate is therefore the point of negotiation, and where a risk premium is attached to the debt instrument to compensate the investor in regards to a return (for the risk taken). As a general rule, the larger the debt is, the higher the risk rate will be (as all other things being equal, a higher debt is harder to pay back). Debtors will also take into consideration the collateral available to the organization (i.e., a valuation of their assets).

Preferred stock is an equity security with properties of both an equity and a debt instrument. It is generally considered a hybrid instrument. Preferred stock represents some degree of ownership in a company, but usually doesn’t come with the same voting rights. In the event of liquidation, preferred shareholders are paid off before the common shareholder, but after debt holders. Preferred stock may also be callable or convertible, meaning that the company has the option to purchase the shares from shareholders at anytime for any reason – usually for a premium – or convert the shares to common stock. Similar to bonds, preferred stocks are rated by the major credit rating companies. Some people consider preferred stock to be more like debt than equity.

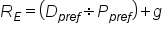

Because preferred stock carries a differing amount of risk than other types of securities, we must calculate its asset specific cost of capital to work into our overall weighted average cost of capital. Similar to debt, this can be a relatively simple process since we can observe values needed as inputs in the market. With preferred shares, investors are usually guaranteed a fixed dividend forever. This is different than common stock, which has variable dividends that are never guaranteed. If the preferred dividend is known and fixed, we can use the following equation to calculate the cost of capital for preferred stock.

This says that the cost of preferred stock is equal to the preferred dividend divided by the preferred stock price, plus the forecasted growth rate. Typically, the dividend is described as a percentage of a predetermined fixed amount, such as par value. These amounts may change based on negotiations, or by virtue of a benchmarked interest rate index.

As a funding source, debt and equity are priced quite differently. While debt relies heavily on default premiums being applied to a risk-free bond rate of interest (the premium usually dependent on the size of the debt compared to the size of the firm), equity isn’t quite as well-defined. As a result, the cost of common equity is often inferred through assessing and comparing it to similar risk profiles, and trying to decipher the firm’s relative sensitivity to systematic (market) risk.

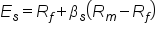

One common tool used in assessing the cost of common equity is the capital asset pricing model (CAPM), which can be described via the following formula:

What this formula is saying is essentially that the cost of equity is equal to the risk-free rate of return plus a premium for the expected risk of investing in the organization’s equity. The variable are defined as follows:

The cost of common equity is essentially the same thing as estimating the expected (or required) return to investors in the stock market. The idea is simply that the higher risk an organization is, the higher the corresponding return should be. As a result, there are countless stock price evaluation strategies and tactics one could use to estimate the cost of common equity from various perspectives. Two of these include the dividend discount model and the Fama-French three-factor model.

| Other Tools to Value Equity | Equation | Description |

|---|---|---|

| Dividend Discount Model |

|

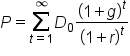

In short, this theory states that a given stock is worth the sum of its future dividend payments, discounted to their present value. This is therefore a model of deriving the present value of future dividend payments, and can be calculated using the formula (assuming no end date). In this calculation, P is the stock price, D is the dividend, g is the (constant) growth rate, r is the constant cost of equity, and t is time. There are a few problems with this method, most notably that a steady and perpetual growth rate that is less than the cost of capital may not be reasonable. Similarly, this model is quite vulnerable to the growth rate. Also, not all stocks pay dividends. |

| Fama-French Three-Factor Model |

|

This valuation model was derived by Eugene Fama and Kenneth French with the intention to include company size and price-to-book ratio with overall market risk. You’ll recognize the first half of this equation as the simple CAPM calculation, while the second half includes SMB (small minus big market capitalization) and HML (high minus low book-to-market ratio) multiplied by coefficients (from linear regression). While this all sounds a bit complicated, the basic premise is to offset the risk calculation with a stronger valuation for a firm’s assets and scale. |

Retained earnings indicate the amount of capital remaining after profits or losses from net income are paid out to investors and shareholders via dividends. Retained earnings are reinvested back into the organization. When organizations create profits, these profits are not always entirely distributed to investors at the end of a reporting period. As a result, these retained earnings can essentially be viewed as a potential funding source for the organization.

No capital comes without costs, however, and the cost of this capital must be taken into account when calculating the weighted average cost of capital (WACC). Retained earnings are included in the WACC equation as equity, as dividends are a component of the return on capital to equity stakeholders, and thus will have a correspondingly weighted influence on the cost of equity.

Understanding the equation to determine the retention ratio adds some clarification for this point:

The dividend payout ratio is a useful addition to the above equation, and is written as:

The relationship between dividends and retained earnings is quite clear when it comes to recognizing the opportunity cost and thus the overall cost of this capital source.

When it comes to the cost of capital, common stock is one of a few options on the table for raising funding. From various debt instruments to preferred stock to common stock, larger organizations tend to diversify funding input to optimize their potential financial leverage. In order to understand the weighted average cost of capital (WACC) of all of these inputs, the cost of each source of debt and/or equity must be determined.

When it comes to issuing common stock, there are both direct and indirect costs to consider.

In terms of literal capital spent, the issuance of new common stock incurs a variety of capital costs both at the initial offering and throughout the process of managing this funding source over time:

In addition to the tangible capital costs involved, there are also a variety of indirect trade-offs that organizations must understand prior to pursuing this source of funding. Indirect costs include:

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM "BOUNDLESS FINANCE" PROVIDED BY LUMEN LEARNING BOUNDLESS COURSES. ACCESS FOR FREE AT LUMEN LEARNING BOUNDLESS COURSES. LICENSED UNDER CREATIVE COMMONS ATTRIBUTION-SHAREALIKE 4.0 INTERNATIONAL.