Table of Contents |

The yield on an investment is the amount of money that is returned to the owner at the end of the term. In short, it’s how much you get back on your investment.

Naturally, this is a number that people care a lot about. The whole point of making an investment is to get a yield. There are a number of different ways to calculate an investment’s yield, though. You may get slightly different numbers using different methods, so it’s important to make sure that you use the same method when you are comparing yields. This section will address the yield calculation methods you are most likely to encounter, though there are many more.

The most basic type of yield calculation is the change-in-value calculation. This is simply the change in value (FV minus PV) divided by the PV times 100%. This calculation measures how different the FV is from the PV as a percentage of PV.

Another common way of calculating yield is to determine the Annual Percentage Rate, or APR. You may have heard of APR from ads for car loans or credit cards. These generally have monthly loans or fees, but if you want to get an idea of how much you will accrue in interest per year, you need to calculate an APR. Nominal APR is simply the interest rate multiplied by the number of payment periods per year.

However, since interest compounds, nominal APR is not a very accurate measure of the amount of interest you actually accrue.

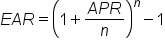

The Effective Annual Rate is the amount of interest actually accrued per year based on the APR. The following formula can be used, where n is the number of compounding periods of APR per year:

IN CONTEXT

You may see an ad that says you can get a car loan at an APR of 10% compounded monthly. That means that the APR is 0.10 and n is 12, since the APR compounds 12 times per year. The effective APR would then be:

That means the EAR is 10.47%.

The EAR is a form of the Annual Percentage Yield (APY). APY may also be calculated using interest rates other than APR, so the following is a more general formula:

The logic behind calculating APY is the same as that used when calculating EAR: you want to know how much you actually accrue in interest per year. Interest usually compounds, so there is a difference between the nominal interest rate (e.g., monthly interest times 12) and the effective interest rate.

The yield of an annuity can be calculated in similar ways to the yield for a single payment, but two methods are most common.

IN CONTEXT

Suppose you have a potential investment that would require you to make a $4,000 investment today, but would return cash flows of $1,200, $1,410, $1,875, and $1,050 in the four successive years. This investment has an implicit rate of return, but you don’t know what it is. You plug the numbers into the NPV formula and set NPV equal to 0.

You then solve for r, which is your IRR. It is not easy to solve this problem by hand. You will likely need to use a business calculator or Excel. When r = 14.3%, NPV = 0, so therefore the IRR of the investment is 14.3%.

Source: THIS TUTORIAL HAS BEEN ADAPTED FROM "BOUNDLESS FINANCE" PROVIDED BY LUMEN LEARNING BOUNDLESS COURSES. ACCESS FOR FREE AT LUMEN LEARNING BOUNDLESS COURSES. LICENSED UNDER CREATIVE COMMONS ATTRIBUTION-SHAREALIKE 4.0 INTERNATIONAL.